Demystifying car rental insurance

So you’re at the car rental pick-up, raring to sit at the wheel and dash to your next destination. While you await your keys, the helpful attendant at the counter has other plans. The inevitable question pops up: ma'am, do you need insurance?

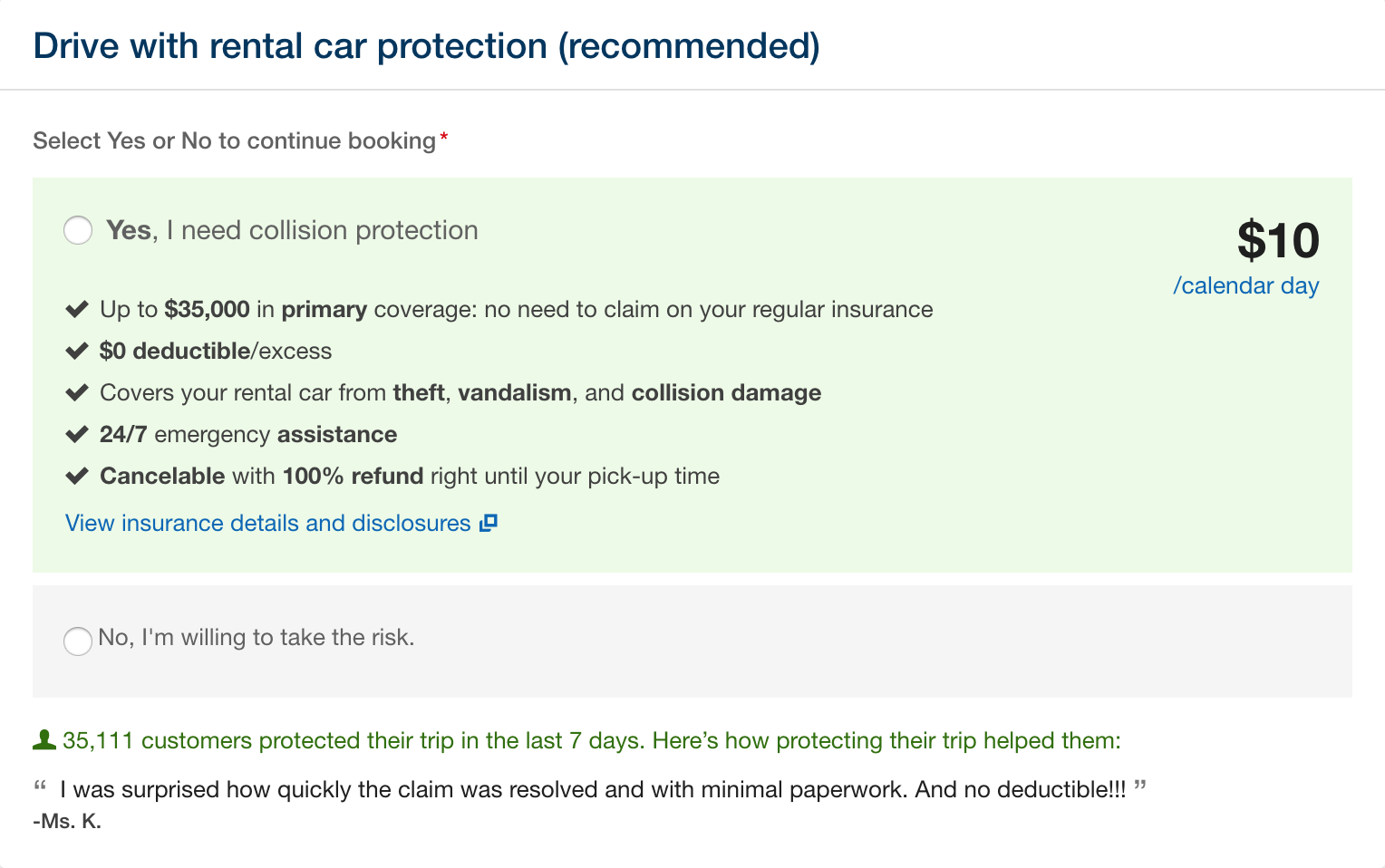

You’re sure you added Travel Guard’s collision damage insurance while booking your rental with Expedia. You tell her as much. But she has more questions; ones with legal-ey terms that you don’t fully understand: liability, supplemental liability, overseas coverage, and so on. Puzzled, you no longer know whether you have the necessary coverage to drive your rental car.

Sounds familiar? Let’s help you clear this confusion.

Collision damage protection

First things first. If you said Yes to Travel Guard’s collision damage protection while booking your car rental with Expedia, you already have collision damage protection. This protection is offered by TravelGuard and it covers you in all US states — when you drive interstate, and even when you drive overseas.

Here’s a quick link to share with the rental agency while picking up your car: Collision Damage Plan. Bookmark it. Even better, download the policy document for your state of residence and keep it handy on your phone or another device.

Keep your key insurance documents handy to make that conversation at the car rental agency easier. Gathering this information is a one-time activity that’ll serve you well whenever you travel or rent a car.

Liability insurance

Many states in the US require you to have a minimum level of liability insurance in order to lawfully drive a car. This minimum coverage varies by state and by the damages caused to others in an accident for which you have legal responsibility.

Do you already have liability coverage?

The Travel Guard Collision Damage Protection plan you bought through Expedia doesn’t include liability protection. However, you might already have liability coverage through other sources:

Personal accident insurance

Your health, life, or auto insurance may already offer a degree of personal accident coverage. Also, neither personal accident insurance nor personal effects insurance is legally required to drive a car.

If your existing insurance already provides personal accident coverage, you can say No to it at the counter.

Additional reading:

Ace the conversation at the counter

Equipped with all that we know now, let's imagine what a sample conversation with your car rental agency attendant might go like:

[…after ID verification and vehicle inspection]

Jargon:unjargon

Car rental insurance comprises several kinds of coverage. Here are the terms you should know:

Get support

Still have questions? Call Travel Guard:

1-855-334-3855